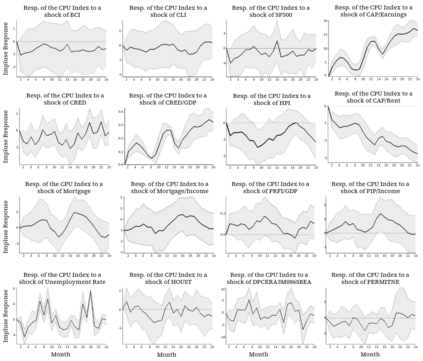

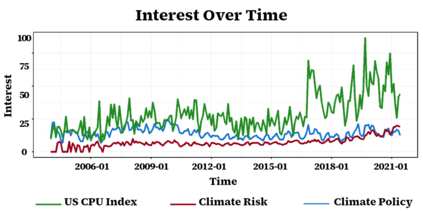

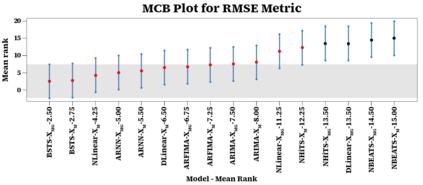

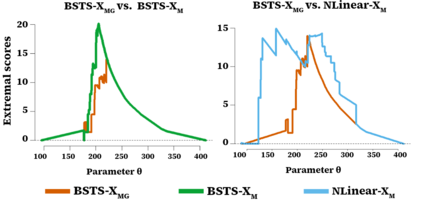

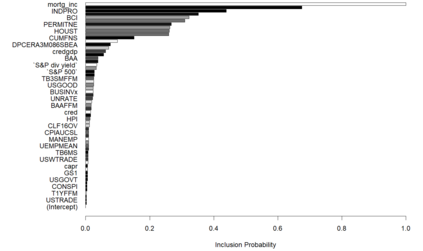

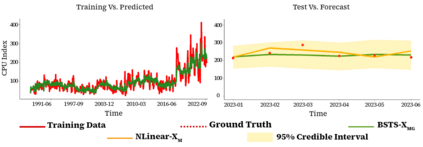

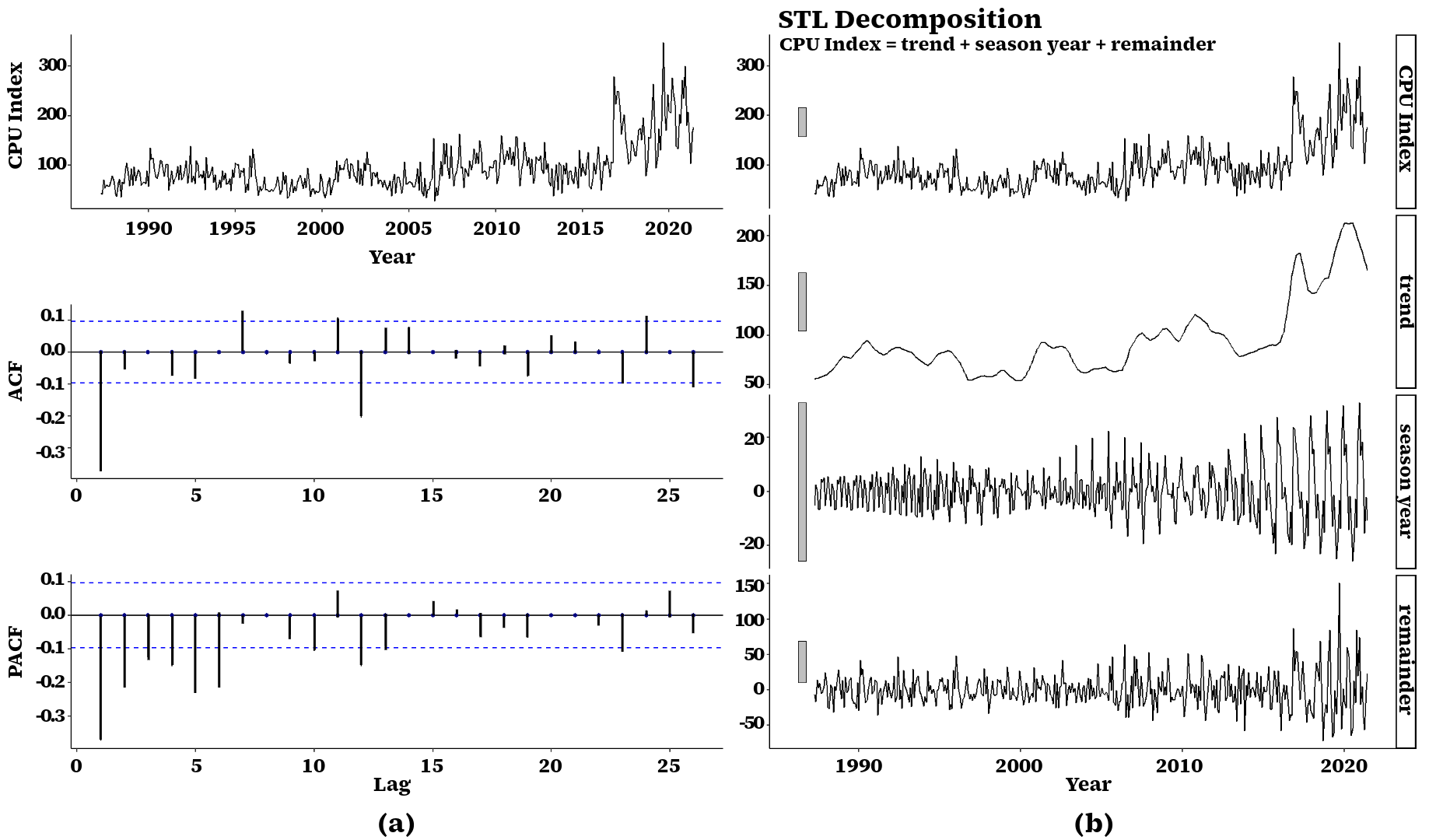

Accurately forecasting Climate Policy Uncertainty (CPU) is critical for designing effective climate strategies that balance economic growth with environmental objectives. Elevated CPU levels deter investment in green technologies, delay regulatory implementation, and amplify public resistance to policy reforms, particularly during economic stress. Despite the growing literature highlighting the economic relevance of CPU, the mechanisms through which macroeconomic and financial conditions influence its fluctuations remain insufficiently explored. This study addresses this gap by integrating four complementary causal inference techniques to identify statistically and economically significant determinants of the United States (US) CPU index. Impulse response analysis confirms their dynamic effects on CPU, highlighting the role of housing market activity, credit conditions, and financial market sentiment in shaping CPU fluctuations. The identified predictors, along with sentiment based Google Trends indicators, are incorporated into a Bayesian Structural Time Series (BSTS) framework for probabilistic forecasting. The inclusion of Google Trends data captures behavioral and attention based dynamics, leading to notable improvements in forecast accuracy. Numerical experiments demonstrate the superior performance of BSTS over state of the art classical and modern architectures for medium and long term forecasts, which are most relevant for climate policy implementation. The feature importance plot provides evidence that the spike-and-slab prior mechanism provides interpretable variable selection. The credible intervals quantify forecast uncertainty, thereby enhancing the model's transparency and policy relevance by enabling strategic decision making.

翻译:暂无翻译