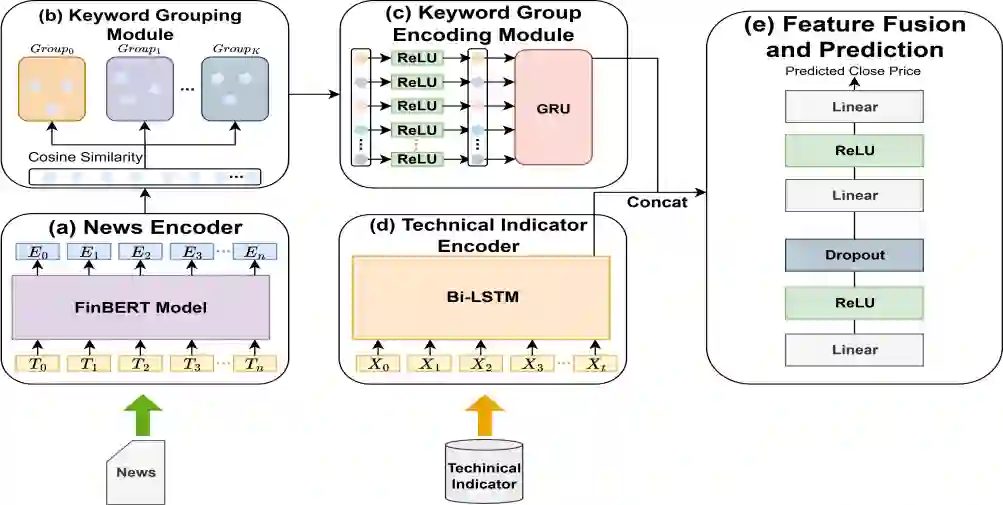

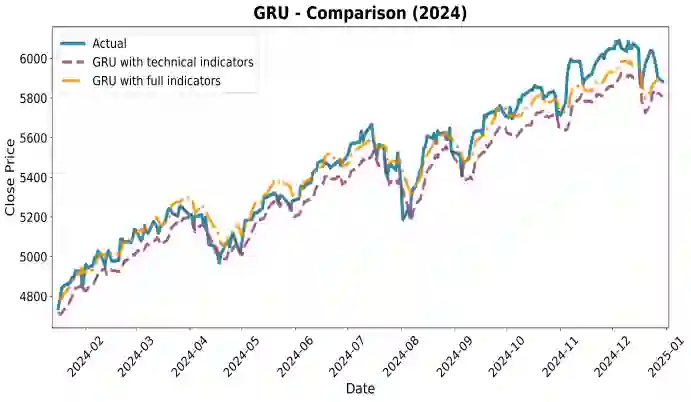

Recent advances in finance-specific language models such as FinBERT have enabled the quantification of public sentiment into index-based measures, yet compressing diverse linguistic signals into single metrics overlooks contextual nuances and limits interpretability. To address this limitation, explainable AI techniques, particularly SHAP (SHapley Additive Explanations), have been employed to identify influential features. However, SHAP's computational cost grows exponentially with input features, making it impractical for large-scale text-based financial data. This study introduces a GRU-based forecasting framework enhanced with GroupSHAP, which quantifies contributions of semantically related keyword groups rather than individual tokens, substantially reducing computational burden while preserving interpretability. We employed FinBERT to embed news articles from 2015 to 2024, clustered them into coherent semantic groups, and applied GroupSHAP to measure each group's contribution to stock price movements. The resulting group-level SHAP variables across multiple topics were used as input features for the prediction model. Empirical results from one-day-ahead forecasting of the S&P 500 index throughout 2024 demonstrate that our approach achieves a 32.2% reduction in MAE and a 40.5% reduction in RMSE compared with benchmark models without the GroupSHAP mechanism. This research presents the first application of GroupSHAP in news-driven financial forecasting, showing that grouped sentiment representations simultaneously enhance interpretability and predictive performance.

翻译:近期金融领域专用语言模型(如FinBERT)的进展使得公众情绪可量化为基于指数的度量,然而将多样化的语言信号压缩为单一指标会忽略上下文细微差异并限制可解释性。为应对这一局限,可解释人工智能技术,特别是SHAP(SHapley Additive Explanations),已被用于识别关键特征。但SHAP的计算成本随输入特征数量呈指数级增长,使其难以适用于大规模文本金融数据。本研究提出一种基于GRU的预测框架,通过GroupSHAP增强,该框架量化语义相关关键词组的贡献而非单个词汇,在保持可解释性的同时显著降低计算负担。我们使用FinBERT对2015年至2024年的新闻文章进行嵌入表示,将其聚类为连贯的语义组,并应用GroupSHAP衡量各组对股价波动的贡献。最终生成的多主题组级SHAP变量作为预测模型的输入特征。对2024年标普500指数进行的单日预测实证结果表明,相较于未采用GroupSHAP机制的基准模型,本方法使MAE降低32.2%,RMSE降低40.5%。本研究首次将GroupSHAP应用于新闻驱动的金融预测,证明分组情感表征能同时提升可解释性与预测性能。